.

Introduced in 2018, the home downsizer scheme allows eligible Australians aged 55 and older to contribute up to $300,000 from the sale of their home into superannuation, outside of normal annual contribution caps.

The idea was simple: improve retirement incomes while freeing up larger homes for younger families.

For eligible couples, up to $600,000 can be taken from their total home proceeds and split equally between their respective super accounts.

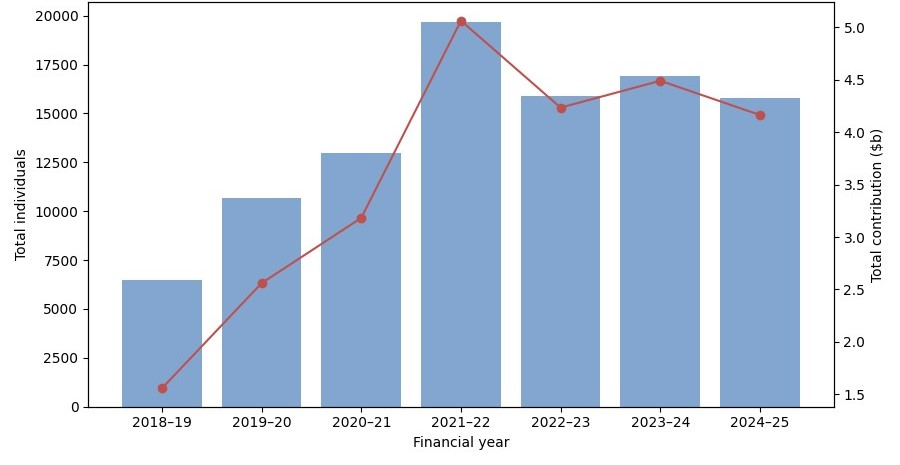

Yet, since peaking in 2021–22 when almost 20,000 people made downsizer contributions totalling just over $5 billion, both the number of contributors and the total value of contributions has declined. Last year 15,800 Australians took advantage of the scheme and contributed a total of $4.16 billion into super – the lowest number in five years.

Total individuals and downsizers contributions by financial year

Source: Australian Tax Office

Which leads to the inevitable question: has interest in home downsizing faded?

Not really. The initial rise in downsizer contributions was powered by people who were already planning to sell. For financially literate retirees with strong super balances and little reliance on the Age Pension, the policy was an obvious opportunity and many moved quickly to take advantage of it.

But a downsizer contribution can only be used once in a lifetime. When those early adopters acted, they permanently exited the pool of potential contributors. By 2021–22, many of the most prepared and motivated households had already made their move.

What followed was a predictable plateau, not a sudden loss of interest.

Many older Australians aren’t selling

Downsizer contributions depend entirely on one thing: older people selling homes. And despite high property prices, many are not willing to make the move.

This was one of the key findings in Vanguard’s How Australian Retires 2025 report, which found that less than 30% of retired Australians have moved or are planning to move into a new home since retiring.

In fact, most retirees see their home as something to hold onto either for life or to pass on as an inheritance. Only 9% of those surveyed considered their home a potential source of retirement funding.

For many older Australians, the family home represents stability, security and independence — benefits that rising prices alone don’t sever.

Interest‑rate uncertainty has bred caution

The past few years have also been marked by sharp swings in interest rates and economic uncertainty. While retirees may carry little debt, they are often more sensitive to volatility than younger households.

Selling into a shifting market raises fears of poor timing, unexpected price falls or difficulty securing suitable replacement housing. In that environment, many retirees have adopted a “wait and see” approach — delaying major decisions, including downsizing.

A lack of supply

Another persistent issue is supply. For downsizing to make sense, retirees need access to smaller, well‑located, accessible homes — ideally within their existing communities.

In many areas, that stock is limited. New apartments may be expensive, poorly designed for ageing residents or poorly located relative to services and family. When suitable housing is scarce, downsizing stalls — and so do downsizer contributions.

The Age Pension remains a silent spoiler

Perhaps the biggest structural brake on downsizer contributions is the government Age Pension.

The family home is exempt from the pension assets test. Superannuation is not. When retirees sell their home and move funds into super via a downsizer contribution, they can inadvertently reduce or eliminate their pension entitlement.

This trade‑off is well understood by financial advisers and deeply felt by retirees near pension thresholds. For many, protecting or maximising the Age Pension outweighs the tax advantages of holding more assets inside super.

A mature scheme meets structural limits

The decline in downsizer contributions largely reflects the reality that downsizing is complex, deeply personal and shaped by pension rules, housing supply and risk aversion.

Early demand has largely been met. What remains is a smaller, steadier flow of people who are ready to move when circumstances align. For most retirees, the decision will continue to hinge on lifestyle, certainty and suitability — not just numbers on personal finances.

For more information on home downsizer contributions including eligibility, contribution limits, and how to make a contribution, visit the ATO website.

Vanguard

11 February 2026

vanguard.com.au

18th-March-2026 |